In the last weeks many Finance Gurus have opined on the likelihood and degree of rate cuts in 2024, while others have commented on the likelihood of sticky inflation remaining above the feds 2% target. So, given that the fed does not usually cut rates when inflation remains higher than expected, who, if anyone, will be right?

⚠️ JUST IN:

— Investing.com (@Investingcom) January 15, 2024

*JP MORGAN'S CEO JAMIE DIMON WARNS INFLATION MAY BE STICKIER, RATES HIGHER, THAN MARKETS EXPECT

DO YOU AGREE? pic.twitter.com/GMiSzzLdj4

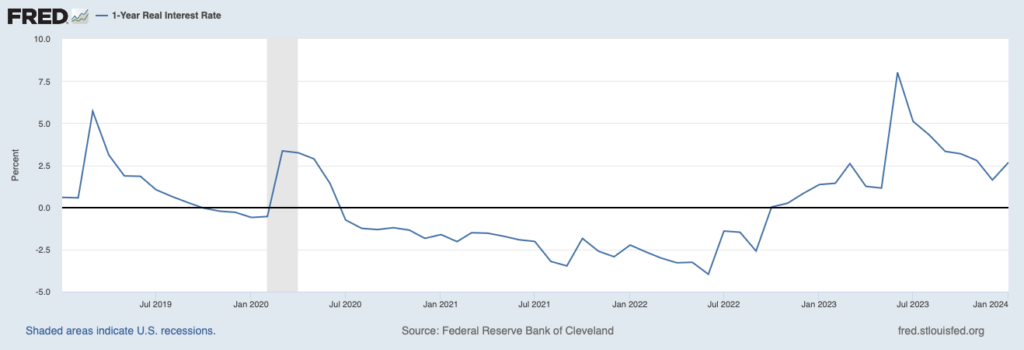

As of Friday, markets are pricing 165bps of rate cuts over the next 12 months, while the Fed’s own SEP projections have 75bps of cuts penciled in. Bill Ackman recently commented that he sees at least 75bps of cuts over the next year because the real rate is too high. To put this in perspective, he explains that if short-term rates are around 5%, 0.75% of cuts would be relatively modest. Striking a similar tone, Paul Tudor Jones noted that he sees a recession starting by early 2024, and therefore believes there is room for short-term rates to fall.

At the same time, Mohamed El-Erian believes disinflation will not continue, and worries cost pressures are building once again. Specifically, El-Erian points to geopolitical tensions in the Red Sea as well as still high wage pressures threatening to keep inflation sticky above 3%. Similarly, Larry Summers commented last week that “the market is underestimating the risk that inflation might return” and pointed to the 5.2% increase in wages. As Summers put it, “my gut is that the market is underestimating the risk of inflation.”

Importantly, Summers goes on to note that whether rates are high enough to bring down inflation depends on whether real rates or the absolute interest rate are what matter, and that this is a topic of debate among economists. Insert joke about economic forecasting. Ackman clearly believes it’s the real rate that matters, and commented that the US can avoid an economic downturn depending on how quickly the fed cuts (which could benefit the stock market “if the fed cuts fast enough to avoid a deep recession”.)

Another line of debate among economists is the question of whether fed tightening has much to do with bringing inflation down at all. In an interview with the FT, Claudia Sham reiterated her view that inflation was driven by supply constraints, and that dampening demand with rate hikes was largely unnecessary. With supply chains healing, Sahm sees inflation cooling towards the 2% and the soft landing “in the bag.” Famous last words in economic forecasting? Sahm dismisses the wage pressure risk cited by Summers and El-Erian with the supply-driven inflation argument, asserting that supply is responsible for inflation rather than stimulus check or wage driven spending power. But even if supply were the overarching driver of inflation, one would think supply-side risks building in the red sea (see Maresk warning) would make 2% inflation less certain than “in the bag?”

Sahm notwithstanding (the gurus have yet to forecast inflation back to the 2% target), will the fed cut rates if inflation remains elevated? FGT would direct you to New York Federal Reserve Chairman John Williams comments, indicating that rates will need to remain restrictive for “some time” as an indication that the Fed now will be patient (at least it doesn’t seem like they are thinking about thinking about hiking rates?.) Indeed, a litany of fed speakers have sought to dial back the rate cut expectations by linking cuts to progress inflation. Even Lael Brainard declined to declare victory over inflation in a recent podcast. One would think that rate cuts being dialed back might be a negative for the stock market, but as some have pointed out, “rate cuts are NOT (necessarily) bullish.” Perhaps ongoing fiscal deficits to the tune of $2T will the keep the real economy (and inflation) alive?

Rate cuts is NOT bullish for the stock market pic.twitter.com/sFtjh7EAGU

— Game of Trades (@GameofTrades_) January 14, 2024

So who will be right? As some have pointed out, it is very difficult to forecast the points of macro inflections in markets and diversification is key. However, FGT would postulate that maybe everyone, including chief stagflation forecaster Nouriel Roubini, will turn out to be right in the sense that in both the recession (stag) and ongoing inflation (flation) outcomes will materialize to some degree and at some point in time. With the ongoing “fiscal situation,” it is hard to feel like the risk of inflation has been vanquished. At the same time, if interest rates remain “higher for longer,” there will certainly be segments of the economy that take issue. Either way, will anybody admit that they were wrong? The forecast says no.